Since the founding of New China, China’s pesticide industry has transformed from a domestic necessity into a globally competitive sector. Through continual reform, strategic investment, regulatory evolution, and international collaboration, China has not only secured its agricultural resilience but has become a major contributor to global crop protection supply chains.

This article highlights the industry’s development timeline, market structure shifts, pricing trends, key players, and international positioning—including updates on export destinations, innovation milestones, and global policy dynamics.

Phase I: Foundation and Early Efforts (1949–1978)

In the early years, China’s pesticide industry operated under a planned economy. Production was concentrated among state-owned enterprises, and the product range was primarily composed of older, high-toxicity compounds such as HCH and DDT. Despite limited infrastructure, these efforts helped mitigate pest-induced crop losses and laid the foundation for future modernization.

Phase II: Reform and Market Activation (1978–1997)

The reform and opening-up policy in 1978 sparked significant momentum in the agrochemical sector. Private and foreign enterprises were allowed to participate, and global chemical leaders like Bayer, DuPont, and Dow entered the Chinese market.

China’s domestic manufacturers began to scale up. By 1994, pesticide exports exceeded imports for the first time, a pivotal moment. In parallel, increased attention to safety and quality led to landmark regulations such as the 1997 Pesticide Management Regulations, which marked a shift from supply-side expansion to compliance and accountability.

Phase III: Environmental Regulation and Global Leadership (1997–2017)

This era marked a shift toward quality improvement and environmental governance. China phased out many high-risk products and actively supported the development of low-toxicity, efficient formulations. By 2010:

- Insecticide market share dropped to 31.4%.

- Herbicides rose to 41%, reflecting broader adoption of conservation agriculture.

- Bio-pesticides and neonicotinoids gained strong market presence.

China joined the WTO in 2001, strengthening global partnerships and export competitiveness. By 2005, China was the world’s largest pesticide producer and exporter. The 19th Party Congress in 2017 elevated ecological goals, reinforcing stricter compliance and green production mandates.

Phase IV: Innovation and Global Integration (2017–Present)

Today’s pesticide sector in China is defined by innovation, global outreach, and sustainability. Major companies are integrating biotechnology, digital tools, and continuous manufacturing systems into their operations. Export competitiveness remains strong, and the focus is shifting toward green chemistry, differentiated formulations, and deeper value chain integration.

Noteworthy Company Developments

Here is a broader view of key players that are driving China’s pesticide industry forward:

Sinochem Holdings / Syngenta Group

One of the most globally integrated and strategically positioned agrochemical groups in China. Through its subsidiaries—Syngenta Crop Protection, ADAMA, and Sinochem Crop Care—Sinochem covers the entire value chain from R&D to global distribution.

- In 2024, Sinochem launched “WeiJing”, a novel acaricide with a unique mode of action, marking a major domestic innovation milestone.

- Has subsidiaries and local teams in Brazil, Argentina, and other regions to tailor solutions for diverse markets.

- Acquired Shenyang Chemical Research Institute, the only domestic full-spectrum pesticide R&D institution.

- Developing low-residue, sustainable pesticides in alignment with global green standards.

Jiangsu Yangnong Chemical (Syngenta Group)

- Expanded glufosinate and pyrethroid production in Yancheng.

- Exports to Brazil, Argentina, and Vietnam.

- Advanced adoption of automated production and formulation precision.

Wynca Group (Zhejiang Xinan Chemical)

- Among top glyphosate exporters worldwide.

- Developing biodegradable adjuvants and greener intermediates.

- Manufacturing presence in Ethiopia and Southeast Asia.

Nutrichem (ChemChina)

- Focused on bio-pesticide fermentation and residue-free formulations.

- Active in FAO and OECD global pesticide regulation initiatives.

- Strong registration portfolio in over 70 countries.

Hailir Pesticides and Chemicals Group

- Launched multiple new formulations and secured major export orders in Southeast Asia and Latin America.

- Enhanced formulation R&D capacity in Qingdao.

Fuhua Tongda Agro-Chemical (Fuhua Group)

- Major producer of chlorantraniliprole and other specialty actives.

- Toll manufacturing partner for multinational companies.

- Key exports: India, Pakistan, South Africa.

Red Sun Group

- Leading supplier of glyphosate, 2,4-D, and chlorpyrifos alternatives.

- Developing green chemistries and export-grade technical materials.

- Active investments in global formulation partnerships.

Jiangsu Huifeng Bio Agriculture

- Recently merged with Jiangsu Lanfeng to scale operations.

- Expanded production of neonicotinoids and systemic fungicides.

- Received green production certifications in 2024.

Trade Policy and Tariff Landscape

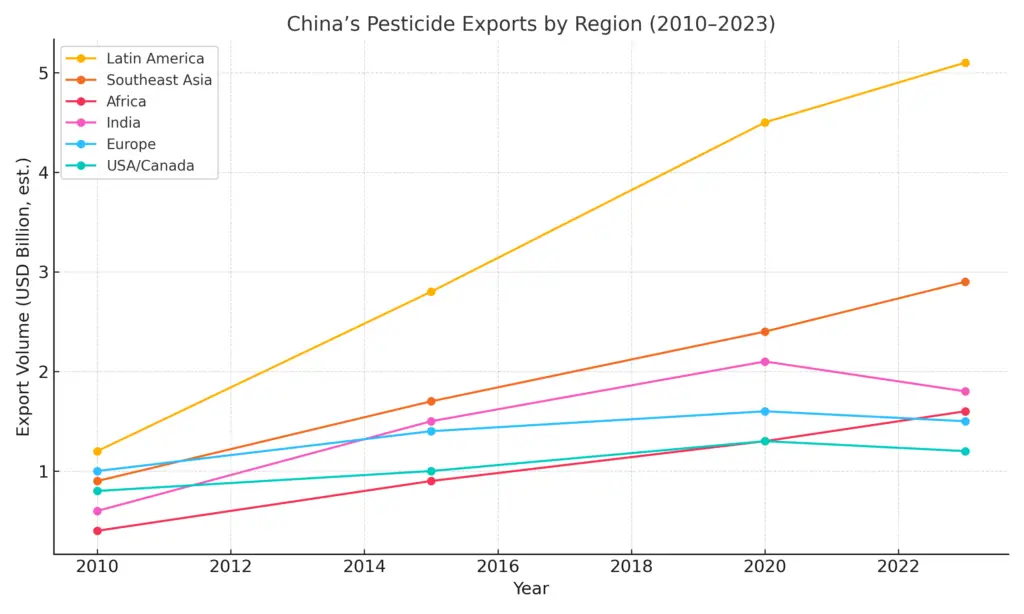

In recent years, Chinese agrochemical exporters have adapted to evolving trade policies. Notably, India imposed anti-dumping tariffs on specific Chinese pesticides, affecting trade volumes.

Chinese companies have responded by:

- Diversifying export destinations (e.g., Latin America, ASEAN, Middle East).

- Establishing overseas formulation plants and regional offices.

- Strengthening registration and compliance in importing countries.

Despite these adjustments, China remains a reliable and cost-efficient source of crop protection products globally.

Market Structure Evolution

| Year | Insecticides (%) | Herbicides (%) | Fungicides (%) | Others (%) |

|---|---|---|---|---|

| 1990 | 70 | 20 | 5 | 5 |

| 2010 | 31.4 | 41 | 7 | 20.6 |

| 2025 (Est) | 25 | 45 | 15 | 15 |

This evolution reflects China’s pivot from conventional actives toward modern, targeted, and lower-toxicity product categories.

Price Trends and Industry Dynamics

Market cycles have influenced pricing of key actives. For example:

- Chlorantraniliprole: RMB 2.4 million/ton → RMB 220,000/ton.

- Glufosinate: RMB 200,000/ton → below RMB 50,000/ton by 2024.

Despite pricing corrections, companies are improving process efficiency and focusing on value-added differentiation rather than volume-driven competition.

Niche Market Opportunities and User-Focused Services

Regional variations in crop types and pest prevalence have created strong demand for tailored solutions in sectors like tea, citrus, greenhouse vegetables, and medicinal herbs.

Simultaneously, end-users increasingly prioritize:

- Application support

- Pest forecasting

- Scientific product usage training

Firms offering these services are gaining trust and building long-term customer loyalty across domestic and international markets.

Barriers to Entry and Compliance Requirements

Modern pesticide production in China requires:

- Heavy investment in safety and environmental technology

- Strong technical teams (chemistry, toxicology, agronomy)

- Advanced equipment for continuous flow, AI-assisted QA, and traceability

This creates high industry entry barriers, which in turn promote sector consolidation and drive quality improvement across the value chain.

Outlook: The Future of China’s Agrochemical Sector

Looking ahead, China’s pesticide industry will likely evolve along three major vectors:

1. Precision Formulation

Customized solutions based on crop structure and localized pest dynamics.

2. Green Technology

Sustained investment in low-toxicity, biodegradable, and fermentation-based products.

3. Global Engagement

Deeper cooperation with global markets, institutions, and supply chains through joint ventures, licensing, and local manufacturing.

Tariff Barriers and Geopolitical Pressures

As China’s dominance in global pesticide exports grows, it has also become a target of rising protectionism and geopolitical trade disputes. One of the most significant recent developments has been India’s imposition of anti-dumping tariffs on several Chinese pesticide products. These measures, aimed at protecting India’s domestic agrochemical manufacturers, have severely impacted Chinese exporters’ access to one of their top foreign markets.

In addition to India, other countries have initiated or considered similar restrictions due to concerns about pricing volatility, product quality, or political tensions. These tariffs are reshaping global trade routes and prompting Chinese firms to diversify export destinations—shifting focus to Latin America, Southeast Asia, and Africa.

Moreover, the U.S.–China trade conflict has introduced uncertainties regarding agrochemical inputs, intermediates, and finished formulations. While most pesticides are not currently subject to the highest tariffs under Section 301, supply chain disruptions and changing bilateral policies have made Western buyers cautious about over-reliance on Chinese sources.

These tariff barriers have forced Chinese producers to re-evaluate pricing strategies, enhance product quality, and accelerate overseas manufacturing setups or joint ventures to bypass trade restrictions—signaling a shift from pure export-driven growth to global production integration.

From National Backbone to Global Pillar

China’s pesticide industry is a cornerstone of global agricultural input supply. From foundational reform to international leadership, the sector reflects China’s ability to innovate, regulate, and scale responsibly.

As global agriculture faces mounting climate and pest challenges, Chinese agrochemical companies are poised to continue making important contributions—through science, sustainability, and global cooperation.

{kind=link}